Introduction: Why Debt Still Matters — Even in 2006

Debt has always been a double-edged sword. It can help you finance a car, pursue higher education, or buy your first home — but when left unchecked, it can quickly become a burden that affects every aspect of your life. Back in 2006, just before the global financial crisis, millions of people were already struggling under piles of credit card bills, student loans, and personal debts. Interest rates were fluctuating, housing prices were soaring, and banks were offering more credit than ever before.

If you’re one of those individuals looking for a fresh start, you’re not alone. Getting out of debt might sound intimidating, but it’s completely achievable with a bit of discipline, consistency, and strategy. In this comprehensive guide, we’ll walk you through five simple yet powerful tips to help you get out of debt and regain financial control — just like people did (or should have done) in 2006.

Let’s dive into practical, realistic steps you can take to regain your financial independence.

Tip #1: Face the Reality — Know Exactly What You Owe

Before you can fix your debt problem, you must acknowledge the full picture. This first step may feel uncomfortable, but it’s the foundation for every other move you make.

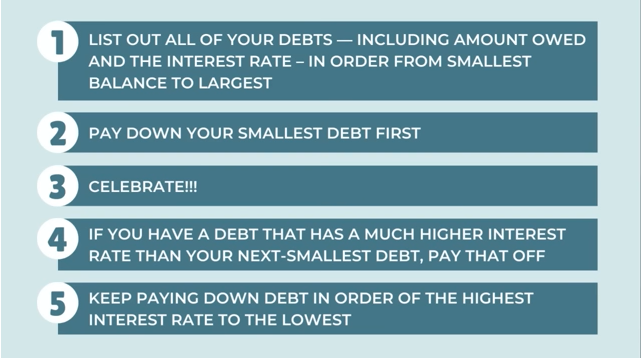

1.1. List All Your Debts

Gather all your bills, loan statements, and credit card summaries. Write down the total amount owed, minimum monthly payment, interest rate (APR), and due date for each account. Whether it’s a student loan, car note, or credit card balance, put it all in one clear, organized list.

1.2. Calculate Your Total Debt

Once you’ve listed everything, calculate the total debt amount you owe. This number might surprise you — but it’s essential to see it in black and white. Don’t panic; remember that awareness is your first weapon.

1.3. Understand Your Interest Rates

High-interest debt (like credit cards) is what traps most people. Knowing your APR helps you decide which debts to tackle first. If your credit card charges 22% interest, while your car loan is only 6%, it’s clear where your focus should go.

1.4. Use Tools for Clarity

In 2006, many people used spreadsheets or manual ledgers to track debts. Today, tools like Mint, You Need a Budget (YNAB), or Credit Karma make it much easier. However, even in 2006 terms, a simple Excel sheet or notebook works just fine.

Facing the numbers is hard, but you can’t fix what you don’t understand.

Tip #2: Create a Realistic Budget and Stick to It

A budget isn’t just about restricting spending — it’s about giving your money direction. In 2006, personal budgeting was becoming more mainstream, and financial gurus like Dave Ramsey and Suze Orman were emphasizing its importance.

2.1. Know Your Income and Expenses

Start by identifying your net income (after taxes) and then track your monthly expenses. Separate essentials like rent, groceries, and utilities from non-essentials like entertainment and dining out.

2.2. Apply the 50/30/20 Rule

A simple rule that works even today:

50% of your income for essentials

30% for wants

20% for savings and debt repayment

Adjust based on your circumstances — if you’re deep in debt, aim to increase your debt payment share to 30% or more.

2.3. Prioritize Needs Over Wants

It sounds simple, but it’s hard to do. In 2006, consumer credit was booming, and buying on impulse was easier than ever. The trick? Learn to distinguish between “I need this” and “I just want this.” Every dollar you save can go toward debt reduction.

2.4. Use Cash Whenever Possible

One of the simplest psychological tricks to control spending is to use cash instead of cards. Handing over physical money makes you more conscious of your spending than swiping plastic.

2.5. Stick to the Plan

Consistency is the real challenge. Review your budget weekly, adjust where necessary, and keep your long-term goal in mind: freedom from debt.

Tip #3: Choose a Debt Repayment Strategy That Works for You

There’s no one-size-fits-all solution when it comes to paying off debt. In 2006, two popular methods — the Debt Snowball and the Debt Avalanche — were already helping people gain momentum.

3.1. The Debt Snowball Method

This approach focuses on paying off your smallest debts first, regardless of interest rate. The idea is to gain motivation as you eliminate debts one by one.

How it works:

List debts from smallest to largest.

Pay minimums on all except the smallest.

Throw every extra dollar you can at that smallest debt.

Once it’s paid, move on to the next one.

This method builds psychological momentum — you see progress faster, which keeps you motivated.

3.2. The Debt Avalanche Method

This method targets high-interest debts first, saving you more money over time.

How it works:

List debts by interest rate (highest to lowest).

Focus all extra payments on the one with the highest rate.

Once paid, move to the next.

While slower emotionally, it’s more efficient mathematically.

3.3. Consolidate or Refinance When Possible

In 2006, credit consolidation companies were booming — some good, some predatory. If you can qualify for a lower-interest personal loan or balance transfer card, it might help simplify and lower your total payments. However, read the fine print carefully to avoid hidden fees.

3.4. Automate Your Payments

Setting up automatic payments prevents missed deadlines and helps build a positive credit history. Even small missed payments can hurt your score, so automation is your friend.

3.5. Celebrate Small Wins

Debt repayment is a long journey. Every time you close an account or reach a milestone — celebrate it (within budget). Motivation is key.

Tip #4: Increase Your Income — Don’t Just Cut Expenses

You can only cut so much, but your earning potential is nearly limitless. In 2006, side hustles weren’t as trendy as they are today, but people were still finding ways to make extra cash — part-time jobs, freelancing, selling used items, and more.

4.1. Take a Part-Time Job or Side Gig

Work evenings, weekends, or online (if you have internet access). Even an extra $200–$300 a month can speed up your debt repayment dramatically.

4.2. Sell Unused Items

Look around your home. Those old electronics, clothes, or collectibles could bring in quick cash through eBay or yard sales — both very popular in 2006.

4.3. Monetize Your Skills

If you’re good at writing, tutoring, fixing computers, or crafting — turn that skill into income. Even small, consistent earnings add up over time.

4.4. Ask for a Raise

Sometimes, your best opportunity is right where you already work. If you’ve been delivering great results, don’t hesitate to ask for a raise. Just be prepared to show why you deserve it.

4.5. Invest Wisely in Yourself

Education, certifications, and skill development pay off. The more you know, the more valuable you become — and the easier it is to increase your income sustainably.

Tip #5: Change Your Financial Mindset for the Long Run

This last tip is the most important of all. Getting out of debt is not just a financial process — it’s an emotional and psychological transformation.

5.1. Stop Relying on Credit Cards

Credit cards can be convenient, but they can also create an illusion of wealth. Commit to paying with cash or debit until your financial situation improves.

5.2. Build an Emergency Fund

Emergencies are what push people back into debt. Start by saving at least $500, then work up to three to six months of expenses. It doesn’t have to happen overnight, but it’s critical.

5.3. Surround Yourself with the Right Influences

Your financial habits are influenced by the people around you. Avoid friends who pressure you to spend money you don’t have. Follow financial educators, read personal finance blogs, or join debt-free communities.

5.4. Reward Yourself Responsibly

When you reach milestones — like paying off a loan — reward yourself modestly. The goal is to reinforce positive behavior without slipping into old habits.

5.5. Visualize Financial Freedom

Imagine what life will be like when you’re debt-free. Picture your bank account growing, the stress melting away, and the sense of empowerment that comes from true financial independence. Visualization can strengthen discipline and motivation.

Bonus Section: Mistakes to Avoid When Getting Out of Debt

Even with a solid plan, it’s easy to fall into traps. Here are some common mistakes to watch for:

Ignoring Your Credit Report: Always check for errors — incorrect balances or late payments can harm your score.

Closing Credit Accounts Too Soon: Keep older accounts open to preserve credit history.

Falling for Debt Relief Scams: Be cautious of companies promising “instant debt forgiveness.”

Not Having a Plan After Debt Freedom: Once you’re out of debt, stay there by budgeting and saving consistently.

Conclusion: Take Control, One Step at a Time

Getting out of debt isn’t just about numbers — it’s about mindset, consistency, and determination. Whether it’s 2006 or 2025, the principles remain timeless. By following these five simple tips — facing your debt, budgeting wisely, choosing the right repayment strategy, increasing your income, and shifting your mindset — you can completely transform your financial future.

Remember: Debt freedom doesn’t happen overnight. It’s a process built on small, daily decisions that move you closer to your goal. Stay patient, stay consistent, and soon you’ll look back and realize — the hardest part was simply getting started.

Word Count:

904

Summary:

Is credit card debt driving you crazy? Spent too much this holiday season?

Well, you�re definitely not alone. Credit card debt is a way of life these days. Especially now, right after the holidays!

For many people, money gets REAL tight this time of year � we need to pay for all the holiday gifts, get ready for tax season�

Ahhhh!

What can you do if debt has taken over your life?

Make getting out of debt your New Year�s Resolution for 2006!

Here are 5 simple …

Keywords:

new years resolution,get out of debt, debt reduction tips,financial advice

Article Body:

Is credit card debt driving you crazy? Spent too much this holiday season?

Well, you�re definitely not alone. Credit card debt is a way of life these days. Especially now, right after the holidays!

For many people, money gets REAL tight this time of year � we need to pay for all the holiday gifts, get ready for tax season�

Ahhhh!

What can you do if debt has taken over your life?

Make getting out of debt your New Year�s Resolution for 2006!

Here are 5 simple tips for getting out of debt. Keeping a New Year�s Resolution is difficult. But if you follow these tips, you�ll be prepared for a prosperous 2006!

1) Write down your goal and make a plan for achieving it!

The first step to getting out of debt is by far the most important � you need to:

� make a commitment to get out of debt

� write it down

� and come up with a plan for reaching it!

Hey, you didn�t get into debt overnight, and you won�t get out overnight, either. But if you want to get out of debt � if you REALLY want to get out of debt, you need to have a plan. And you need to stick with it.

2) Seriously consider using a debt reduction program

If you have the discipline to get out of debt on your own, without any help, then good for you! But if you�re like most people, a little help will go a long way. Here are a few debt reduction programs to consider:

� Credit counseling: If you have high interest rates on your credit cards, working with a non-profit company will help you lower those high rates, and combine your credit card bills into one lower monthly payment � which means more of your money will go towards reducing your debt!

� Debt consolidation loan: If you own a home, you can consider taking out a home equity loan to pay off all your credit card bills, lower you interest rates, and possibly deduct the interest on your taxes (but check with your tax professional on this one).

� Debt settlement: If nothing else is working, and your debt is still overwhelming, then you should consider debt settlement. This is a more aggressive approach, and is not right for everyone, but if you�re considering bankruptcy, this is a good option. You can pay off all your credit card bills at a savings of 40-60%, and get out of debt much quicker.

3) Start fixing your credit problems

Many people think that anything that goes on your credit report stays there for 7 years. Well, that�s not always true. I got a bunch of negative credit items off my credit report � all I did was get a copy of my credit report, and ask the credit bureaus to remove the �bad stuff�. In just a few months, my credit was almost back to normal. There�s nothing that says we must pay for our mistakes forever (or even for 7 years)!

4) Cut down your monthly expenses

If you overdid the spending in 2005, then it�s time to cut out all the expenses you don�t need, and use the money you save to pay off your credit card bills. Take a look at your checking and savings account statements, your credit card statements, and your monthly bills. Then start looking for things to cut. I know, I know, it�s hard to live without cable TV, cell phones, internet access, the morning paper, weekend dinners and entertainment. BUT DO IT ANYWAY � at least until you get your debt back under control!

5) Make some extra spending money

Sometimes making more money is the best answer! There are lots of ways to make money � selling some of your valuables, getting a part-time job, starting your own business. Despite some of the ads you read, there�s no really secret to making money � you just need to find something you like to do, and work hard at it!

6) Think positive!

OK, there were only supposed to be 5 tips, but this one is the best one � no matter how hard life can get, no matter how much debt you have, the one thing in life you can control the most is how you think. So rather than focusing on what you don�t have, be thankful for all that you do have. Nobody dies wishing they had made more money or worked longer. But many people do regret all the fun and meaningful things THEY DID NOT DO! So make some time to have fun, think positive, and find little ways to enjoy life EVERY SINGLE DAY you are here on plant Earth!

Wondering what makes me an expert on debt? Well, I lived through it. I know what it feels like to struggle. And I know what it feels like to overcome financial problems. There�s nothing special about me. I work at a college, so I don�t make a heck of a lot of money. I didn�t win the lottery. And no rich relatives left me a pile of money.

I just learned a few simple strategies � actually, I learned the 5 tips you just read about � and stuck with them until my life changed for the better.

And you can, too � just follow the tips above, believe in yourself, and DON�T LET ANYONE OR ANYTHING STOP YOU FROM REACHING YOUR GOALS in life!

Tinggalkan Balasan