Debt is a persistent companion for many households, slowly eroding financial stability, peace of mind, and long-term wealth. Unlike temporary financial setbacks, unchecked debt can accumulate over years, creating a compounding burden that affects every aspect of life. Whether it’s credit card balances, personal loans, mortgages, or student debt, the cumulative effect can be staggering.

Breaking free from this cycle requires awareness, planning, and disciplined action. By understanding how debt grows over time, recognizing its psychological and financial impact, and implementing concrete strategies, you can regain control of your finances and stop debt from eating away at your life.

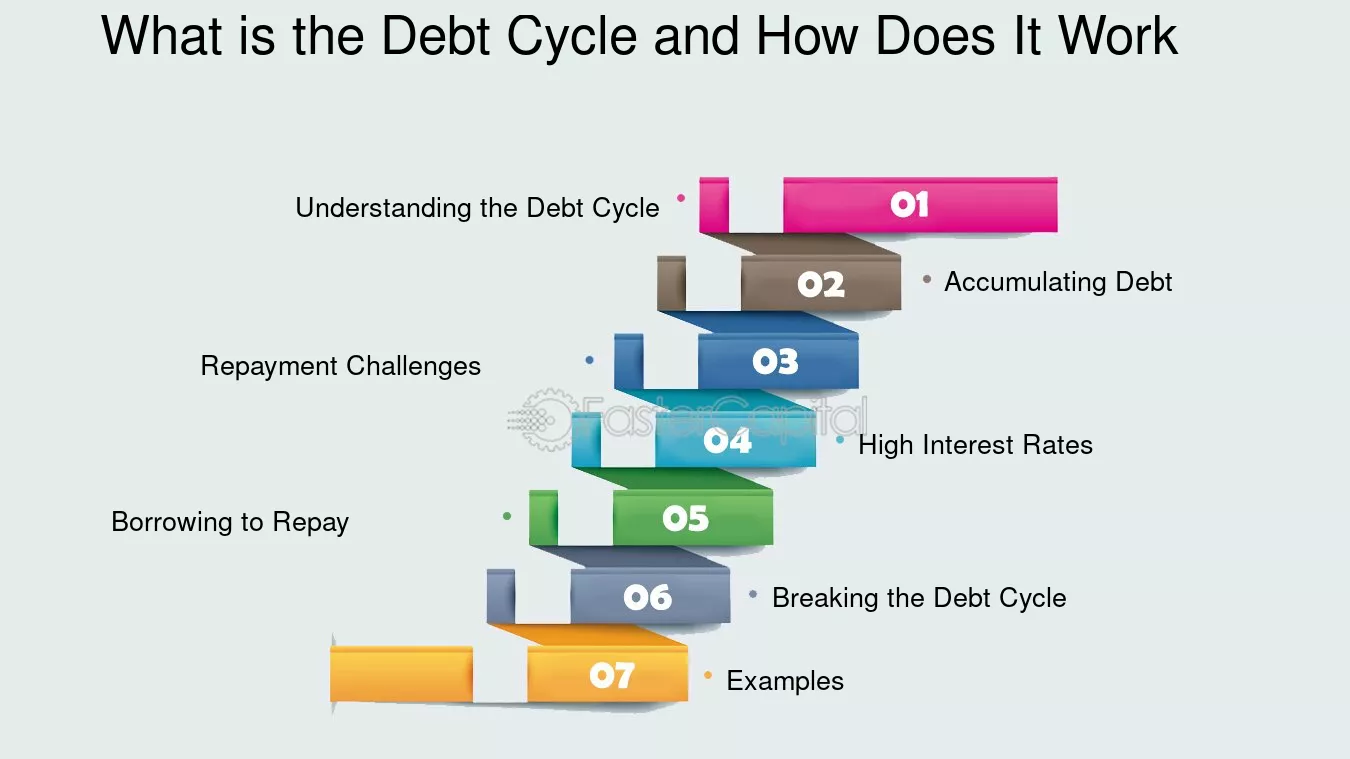

Understanding the Debt Cycle

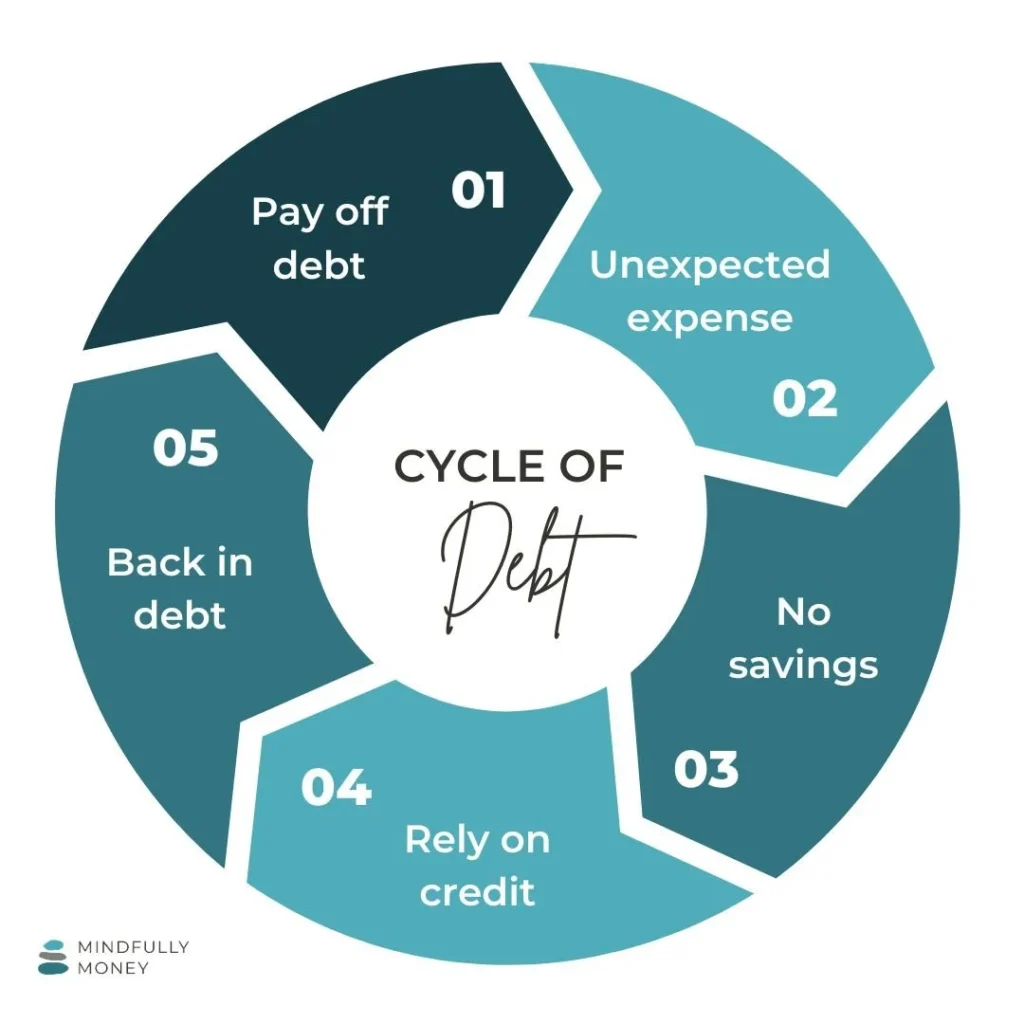

1. How Debt Accumulates Over Time

Debt is not just the initial borrowing—it is the interest, fees, and penalties that compound over months and years. Key factors that contribute to long-term debt accumulation include:

- High-Interest Rates – Credit cards and payday loans can double or triple the amount owed if balances are not paid promptly.

- Minimum Payments – Paying only the minimum prolongs repayment and increases total interest.

- Repeated Borrowing – Taking new loans to cover old debts creates a snowball effect.

- Lifestyle Inflation – Spending beyond your means as income increases adds additional pressure.

The result is a cycle where debt grows faster than your ability to repay, leading to stress and financial insecurity.

2. The Psychological Impact of Debt

Debt can affect mental and emotional well-being:

- Stress and Anxiety – Constant worry about bills and payments.

- Guilt and Shame – Feeling personal failure for being in debt.

- Depression – Long-term financial strain can affect overall mood and motivation.

- Relationship Strain – Money disputes are one of the leading causes of domestic tension.

Understanding the psychological component is essential for breaking the debt cycle.

The Dangers of Long-Term Debt

Long-term debt has far-reaching consequences:

- Financial Drain – High interest payments reduce money available for savings, investments, and essentials.

- Limited Opportunities – Debt can restrict your ability to invest, purchase a home, or fund education.

- Lower Credit Score – Persistent debt increases credit utilization and lowers your score.

- Increased Vulnerability – Emergencies or unexpected expenses become more difficult to handle.

- Compounding Interest – Unmanaged debt grows exponentially, making repayment harder over time.

Recognizing these dangers motivates proactive action.

Steps to Stop the Debt Cycle

1. Assess Your Debt Situation

- Make a comprehensive list of all debts, including balances, interest rates, and monthly payments.

- Understand which debts are growing fastest and which are most critical.

- Prioritize repayment based on interest rates or outstanding balances.

2. Create a Budget and Track Expenses

- List all sources of income and essential expenses.

- Allocate a fixed portion for debt repayment each month.

- Track spending to identify areas where costs can be reduced.

A clear budget allows you to channel resources effectively and prevent further debt accumulation.

3. Prioritize Debt Repayment

Two common strategies:

- Avalanche Method – Focus on paying debts with the highest interest rates first, reducing overall interest paid.

- Snowball Method – Pay off smaller debts first to gain psychological momentum and motivation.

Both methods are effective; choose the one that fits your financial discipline and mindset.

4. Stop Adding New Debt

- Avoid using credit cards for non-essential purchases.

- Delay large discretionary spending until debts are under control.

- Use cash or debit to manage day-to-day expenses.

Ceasing new debt is critical to breaking the cycle.

5. Consider Consolidation or Negotiation

- Debt Consolidation – Combine multiple debts into one loan with a lower interest rate.

- Negotiation – Some creditors may reduce interest rates or offer flexible repayment plans.

- Refinancing – For mortgages or auto loans, refinancing can reduce monthly obligations.

Strategic financial tools help manage debt more efficiently.

Building an Emergency Fund

Unplanned expenses often trigger new debt. An emergency fund provides a buffer:

- Save 3–6 months of living expenses in a separate account.

- Use the fund only for genuine emergencies.

- Regular contributions prevent reliance on high-interest credit during unexpected events.

An emergency fund is essential for financial stability and stopping debt recurrence.

Financial Mindset and Discipline

1. Shift from Spending to Saving

- Prioritize savings over unnecessary consumption.

- Delay gratification and focus on long-term financial goals.

2. Educate Yourself About Debt

- Learn how interest works and the impact of compounding.

- Understand the terms and conditions of loans and credit products.

3. Set Clear Goals

- Short-term: Reduce high-interest credit card debt.

- Medium-term: Consolidate loans and build emergency savings.

- Long-term: Achieve debt freedom and invest for financial growth.

Clear goals keep you focused and disciplined.

4. Involve Family Members

- Discuss spending habits and financial priorities openly.

- Encourage shared responsibility for debt repayment.

- Avoid hidden borrowing or overspending that can worsen the cycle.

Practical Debt Prevention Strategies

- Track Every Dollar – Small, unnoticed expenses can accumulate into significant debt.

- Limit Credit Card Use – Use for emergencies or planned purchases only.

- Automate Payments – Avoid late fees and penalties by setting up automatic payments.

- Negotiate Bills – Utilities, insurance, and subscriptions can sometimes be reduced.

- Live Below Your Means – Adjust lifestyle according to income rather than desire.

- Use Windfalls Wisely – Tax refunds, bonuses, or gifts should go towards debt repayment or savings.

These strategies reduce financial vulnerability and prevent new debt.

Psychological Strategies to Break the Cycle

- Visualize Debt Freedom – Imagine life without the burden of interest and obligations.

- Reward Milestones – Celebrate debt repayment achievements to maintain motivation.

- Avoid Comparison – Don’t compare your financial situation to others; focus on your progress.

- Practice Mindfulness – Reduces impulsive purchases and promotes conscious spending.

Mental strategies reinforce practical steps and maintain long-term discipline.

Professional Assistance

Sometimes professional help is necessary:

- Financial Advisors – Provide personalized plans and strategies.

- Credit Counselors – Assist with budgeting, debt management, and repayment plans.

- Debt Relief Programs – Offer consolidation or negotiation services with creditors.

Seeking help is a proactive step, not a sign of failure.

Long-Term Strategies for Financial Health

- Invest for the Future – Once debt is under control, focus on wealth-building.

- Maintain Good Credit – Responsible borrowing keeps access to favorable loans if needed.

- Review Financial Plans Annually – Adjust based on income changes, goals, and market conditions.

- Educate Continuously – Stay informed about personal finance, interest trends, and investment strategies.

Long-term planning ensures that debt does not resurface and financial growth continues.

Conclusion

Debt can slowly eat away at your finances, peace of mind, and opportunities if left unmanaged. However, the cycle can be stopped with awareness, discipline, and strategic action.

Key steps to break the debt cycle include:

- Assessing and understanding your current debt.

- Creating a detailed budget and tracking expenses.

- Prioritizing debt repayment through methods like avalanche or snowball.

- Preventing new debt by controlling spending and credit usage.

- Building an emergency fund to handle unforeseen expenses.

- Adopting a disciplined financial mindset and involving household members.

- Seeking professional assistance if necessary.

- Planning for long-term financial health and growth.

By following these strategies, you can regain control over your finances, prevent debt from compounding, and ensure long-term stability and peace of mind. Debt doesn’t have to be a permanent drain—discipline, planning, and action can stop the cycle and create financial freedom.

Over abundance of debt can totally creep up from out of nowhere for many people and when that does occur it can often times be very overwhelming for many. It is so very important for everyone to keep in mind how very important it is to always try and steer clear from too many unwanted debts because all that leads to is stress, stress and more stress, which far too many of us know a little bit about, or maybe even a whole lot about.

If your debt condition is currently driving you up the wall then you already know how devastating it can turn out to be, so make sure even you continue to read throughout this article because you might find it to be very helpful, as well as beneficial to you. Your debt responsibilities will become a priority and you will finally have the opportunity to get yourself and your financial standing on the path that it should be, which is where most of us only dream of ever having it.

It is your responsibility as an adult to start thinking more about the future of yourself and the future of your children as well, which I am certain most of you already have given thought to. Finding out more about the importance of debt relief will change the way you live your life each and everyday that passes. You will be much more conscious about the different things you are spending your money on, as well as the amount of money you are trying to save each month, if any at all.

Your money should be very helpful to you but if you constantly are finding out that your money seems to be going nowhere except to pay off your monthly debt, whenever you are able to, then perhaps something within your budget could need some improvement, just a little bit. I am hoping that by gathering up enough debt information you will be able to finally get your finances under some sort of control and stop increasing your debt each month.

Debt can be controlled by just making a few small changes in your lifestyle each month and I am not at all talking about anything major that would affect your entertainment each month or fun times with friends. Just slow down and pay closer attention to what is coming out of your wallet and if you can continue this type of responsible behavior over a period of time then you will definitely begin noticing slight changes in the amount of extra money you have each month.

If all else fails, talk to a professional about your current debt condition and there is surely to goodness somebody out there more experienced and knowledgeable than you are, who could really help to turn your world around, by providing you with the same knowledge that they are aware of because of studying it over a period of time throughout life. This knowledge can be a lifesaver and can really brighten the outlook of your future, as well as your children’s and grandchildren’s future. Good luck.

Tinggalkan Balasan